When History Chooses Irony Over Justice

History has an uncanny habit of composing ironies that no playwright could imagine and no satirist could improve. For over seven decades, independent India has sought, with varying degrees of diplomatic restraint and moral conviction, the return of the Kohinoor Diamond—a priceless jewel whose journey from the Indian subcontinent to the British Crown remains inseparable from the larger history of colonial conquest and imperial appropriation. Britain has consistently resisted those appeals, sheltering behind legal doctrines, historical interpretations and museum diplomacy.

Yet history now appears prepared to script a different form of restitution.

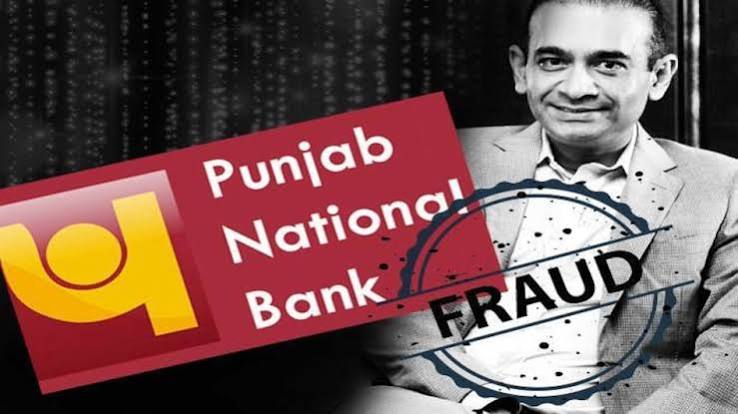

If Britain is unwilling to part with the Kohinoor, it may soon return another “diamond”—not one that adorned the imperial Crown, but one who allegedly engineered one of the largest banking frauds in the history of independent India. Having exhausted successive appeals before British courts and sought relief through the European legal process, Nirav Modi appears to be approaching the end of his long legal sanctuary. The ancient Persian maxim remains profoundly relevant: “Khuda ke ghar mein der hai, andher nahin”—there may be delay in the house of God, but never injustice.

The symbolism is irresistible. One diamond left India during the age of empire. Another may return during the age of global financial accountability. One sits behind bullet-proof glass as a symbol of imperial splendour. The other may exchange London’s elegance for the austere confines of an Indian prison.

History occasionally writes satire with remarkable precision.

Beyond One Man: The Failure of an Entire System

The Nirav Modi affair should never be reduced to the story of an individual fugitive or a sensational criminal prosecution. That would trivialise one of the gravest institutional failures witnessed by India’s financial architecture in recent decades. Financial frauds involving thousands of crores do not emerge overnight. Nor are they accomplished by individual brilliance alone.

They flourish when systems designed to prevent them gradually cease to function. The Punjab National Bank fraud was therefore not merely a banking scandal. It represented a convergence of corporate greed, institutional complacency, bureaucratic opacity, regulatory fragmentation, technological vulnerability and administrative inertia. It exposed uncomfortable truths about governance within India’s banking sector and raised disturbing questions regarding accountability in institutions entrusted with safeguarding public money. Large financial crimes rarely have a single author. They resemble orchestral performances where multiple instruments fall silent simultaneously.

The Glitter Behind the Glass

Diamonds have traditionally symbolised permanence, purity, prestige and prosperity. Ironically, the very industry associated with rarity and refinement became the setting for one of India’s most spectacular episodes of financial deception. The alleged fraud did not depend upon sophisticated cyber warfare, artificial intelligence or complex digital manipulation. Its success lay in exploiting something far older than technology itself—the enduring alliance between human greed and institutional complacency.

While the ordinary citizen patiently submits documents for a modest housing loan, while farmers struggle to secure seasonal agricultural credit, while pensioners anxiously await loan approvals and small entrepreneurs repeatedly visit bank branches to satisfy procedural requirements, enormous financial facilities allegedly flowed through institutional channels with astonishing ease. The contrast was neither accidental nor merely administrative. It represented a deeper asymmetry within India’s financial culture. The poor often encounter procedures. The powerful frequently encounter discretion.

The Anatomy of an Extraordinary Fraud

The operational mechanism behind the fraud has now become part of banking history. Officials within Punjab National Bank allegedly issued fraudulent Letters of Undertaking (LoUs) through the international SWIFT messaging system without recording those liabilities in the bank’s Core Banking Solution (CBS). That omission was neither technical nor trivial. It effectively created two parallel financial realities.

One existed before international banks that honoured these guarantees in good faith.

The other existed within the bank’s own accounting framework, where the liabilities simply did not officially appear.

International lenders believed sovereign-backed banking assurances existed.

Internal banking records suggested otherwise.

The fraud therefore thrived in the invisible space between technology and governance.

It was less a triumph of criminal sophistication than an extraordinary collapse of institutional discipline

When Every Watchdog Sleeps

Perhaps the most disturbing aspect of the scandal lies not in its magnitude but in its duration.

Modern banking operates through multiple concentric circles of oversight.

Branch managers supervise operations.

Concurrent auditors examine daily transactions.

Internal auditors periodically review compliance.

Statutory auditors independently certify financial statements.

Risk management departments monitor exposure.

Vigilance wings investigate irregularities.

Boards of Directors exercise strategic oversight.

The Reserve Bank of India regulates systemic stability.

Government ministries supervise public sector banks.

Each institution represents one defensive wall protecting public deposits.

Yet somehow, every wall developed invisible cracks.

Warnings either failed to emerge, failed to travel or failed to provoke corrective action.

Such institutional silence inevitably generates uncomfortable questions.

Can fraud of this magnitude continue for years merely because procedures failed?

Or does prolonged procedural failure eventually become indistinguishable from institutional connivance?

The distinction is uncomfortable. The question is unavoidable.

Public Banks, Private Kingdoms

Public Sector Banks occupy a unique constitutional position within India’s economic framework. Their capital originates substantially from taxpayers. Their deposits represent the accumulated savings of millions of ordinary citizens. Their credibility rests ultimately upon sovereign confidence.

They are therefore not merely commercial institutions.

They are custodians of public trust.

Yet repeated banking scandals reveal a recurring paradox.

A marginal farmer who defaults on a modest crop loan receives repeated notices.

A retired employee missing housing loan instalments risks recovery proceedings.

A small entrepreneur seeking working capital must satisfy endless documentation.

Meanwhile, influential borrowers have repeatedly succeeded in obtaining extraordinary financial accommodation.

The asymmetry undermines both banking discipline and democratic morality.

When ordinary citizens perceive unequal treatment, confidence begins to erode.

And confidence—not currency—is the true foundation upon which every banking system ultimately rests.

As the economist John Kenneth Galbraith observed, “The process by which banks create money is so simple that the mind is repelled.” Equally simple, perhaps, is the process by which institutions lose public confidence.

Once lost, trust is far more difficult to recover than money itself.

From Harshad Mehta to Nirav Modi: A Repeating Cycle

The Nirav Modi affair did not emerge in isolation. It belongs to a long and uncomfortable chronology of financial scandals that have periodically shaken India’s economic institutions. The securities scam engineered by Harshad Mehta in the early 1990s exposed weaknesses in the banking and government securities markets. The Ketan Parekh episode demonstrated how speculative excesses could manipulate capital markets with alarming ease. The Satyam corporate fraud revealed that even celebrated corporate governance could rest upon fabricated accounts. The Vijay Mallya loan defaults, Mehul Choksi’s escape and finally the Punjab National Bank fraud collectively exposed another disturbing reality—that economic offenders increasingly operated across jurisdictions, exploiting legal complexity, regulatory delays and international mobility.

Each scandal generated committees, inquiries, legislative amendments and solemn assurances that “such incidents will never recur.” Yet the recurrence itself suggests that reforms have often been reactive rather than transformative. India has repeatedly repaired the symptoms while leaving structural vulnerabilities substantially intact.

The Political Economy of Public Banking

Public sector banks were established not merely as commercial enterprises but as instruments of national development. Following bank nationalisation, they became vehicles for financial inclusion, agricultural credit, industrial expansion and social welfare. They financed India’s Green Revolution, infrastructure development, rural employment and the growth of small and medium enterprises.

Over time, however, commercial prudence increasingly came under pressure from competing political, administrative and corporate interests. Lending decisions occasionally reflected influence rather than rigorous risk assessment. Loan restructuring, evergreening of stressed assets and repeated extensions sometimes postponed the recognition of underlying problems rather than resolving them.

The consequence was predictable. While genuine entrepreneurs encountered increasing procedural hurdles, influential borrowers often negotiated extraordinary flexibility. This imbalance gradually weakened credit discipline and contributed to the accumulation of large Non-Performing Assets.

Crony Capitalism and Moral Hazard

Economic development demands vibrant entrepreneurship. It does not justify privileged access. The distinction between legitimate enterprise and crony capitalism is fundamental. Markets reward innovation; cronyism rewards proximity to power. The Nirav Modi episode reignited concerns regarding the relationship between political influence, corporate privilege and institutional discretion. Whether actual or perceived, such proximity damages the credibility of financial governance. Citizens begin to believe that economic opportunity is determined less by enterprise than by access. This perception itself becomes economically dangerous.

As Adam Smith cautioned centuries ago, markets flourish only where justice is impartially administered. When rules appear negotiable for the influential but inflexible for ordinary citizens, confidence in both capitalism and governance begins to weaken.

The Invisible Victims

The arithmetic of financial fraud is deceptively simple.

Thousands of crores are diverted.

Investigations commence.

Properties are attached.

Assets are auctioned.

Court proceedings continue for years.

Yet public discourse often overlooks those who ultimately bear the cost.

Depositors lose confidence.

Taxpayers finance recapitalisation.

Honest borrowers face tighter lending norms.

Exporters encounter additional compliance burdens.

Small businesses struggle to obtain working capital.

Economic growth absorbs the hidden shock.

Every major banking fraud therefore produces millions of invisible victims who never appear in charge sheets or courtroom proceedings.

When trust declines, the cost of capital rises.

When confidence weakens, investment hesitates.

When banks become excessively cautious, productive sectors suffer.

The economic consequences extend far beyond the balance sheet of a single institution.

Technology Without Integrity

Modern banking increasingly depends upon digital integration, artificial intelligence, automated compliance and real-time surveillance.

Yet technology is not a substitute for ethics.

The fraudulent use of the SWIFT messaging platform without corresponding entries in the Core Banking System illustrated a painful truth: sophisticated software cannot compensate for compromised human judgment.

Algorithms process information.

They cannot replace integrity.

Digital platforms accelerate transactions.

They cannot create accountability.

Technology magnifies efficiency, but it magnifies dishonesty with equal speed when institutional controls collapse.

The lesson extends well beyond banking.

Every technological revolution must ultimately be accompanied by an ethical revolution.

Otherwise, innovation merely increases the scale of misconduct.

Audit Without Courage

Auditing occupies a sacred place within financial governance.

Its purpose is not merely to verify arithmetic but to question improbabilities.

An auditor’s first responsibility is professional scepticism.

Large frauds therefore compel equally large questions regarding the effectiveness of concurrent audits, internal audits, statutory audits and inspection mechanisms.

Were warning signals overlooked?

Were exceptions rationalised?

Did procedural compliance gradually replace substantive scrutiny?

History demonstrates that catastrophic financial collapses—from Enron in the United States to banking crises across Europe—rarely occurred because auditors lacked technical competence. More often, they failed because institutional independence gradually yielded to organisational comfort. Audits become meaningful only when they possess both competence and courage.

Enforcement: Reactive Rather Than Preventive

India possesses an impressive institutional architecture to combat financial crime. Investigative agencies, specialised economic intelligence units, banking regulators and enforcement authorities collectively constitute an extensive framework. Yet major economic offenders have repeatedly managed to leave the country before decisive legal intervention.

This recurring pattern demands honest introspection.

Effective governance is measured not merely by successful extradition but by successful prevention.

Investigations after departure may satisfy public outrage.

Preventive vigilance before departure protects the Republic.

As Warren Buffett famously observed, “Only when the tide goes out do you discover who has been swimming naked.”

Financial crises merely expose weaknesses that already existed beneath the surface.

They do not create them.

The challenge before India, therefore, is not simply to recover fugitives but to ensure that institutions identify extraordinary financial irregularities long before economic offenders acquire airline tickets.

Extradition: Justice Beyond Borders

Economic crime has become increasingly transnational.

Money moves across jurisdictions in seconds, while legal systems often move at the pace of decades. Shell companies, tax havens, layered transactions, offshore trusts and multiple citizenships have transformed financial fugitives into global litigants. Extradition is therefore neither a diplomatic favour nor a political spectacle; it is a painstaking judicial process requiring evidence, reciprocity and adherence to international human rights standards.

The proceedings involving Nirav Modi have illustrated this complexity. British courts have examined the admissibility of evidence, prison conditions, fair trial guarantees and human rights considerations before deciding upon extradition. Such scrutiny reflects the rule of law rather than reluctance. Nevertheless, prolonged litigation also demonstrates how wealth can purchase time, if not necessarily immunity.

Justice delayed may still prevail, but justice delayed also carries enormous economic and institutional costs.

Britain’s Curious Restitution

The symbolism remains too striking to ignore.

For generations, India has sought the return of the Kohinoor as a matter of historical justice. Britain has consistently maintained that the circumstances surrounding its possession are legally settled. The debate continues to evoke questions of colonial morality, cultural ownership and historical memory.

Ironically, Britain may now return another “diamond” whose value lies not in carats but in cautionary lessons.

One diamond left India during colonial expansion.

Another may return under the weight of criminal prosecution.

One represented imperial extraction.

The other symbolises financial extraction.

One enriched an empire.

The other allegedly impoverished public confidence.

One occupies a royal display case.

The other may soon occupy the dock of an Indian courtroom.

History has an extraordinary ability to compose metaphors that no novelist could improve.

The Cost of White-Collar Crime

Street crime evokes immediate public outrage because its consequences are visible.

White-collar crime, however, often unfolds silently.

No shattered windows.

No public violence.

No dramatic police chases.

Yet its consequences are vastly more destructive.

When thousands of crores disappear from the banking system, schools remain unfunded, hospitals remain understaffed, infrastructure projects slow down and productive enterprises struggle to obtain affordable credit.

The ultimate victim is not merely the lending institution.

It is the ordinary taxpayer whose money recapitalises distressed banks.

It is the pensioner whose savings depend upon institutional stability.

It is the young entrepreneur denied timely finance because banks become excessively cautious after every scandal.

Economic offences therefore constitute not merely financial crimes but assaults upon national development.

As Chanakya observed in the Arthashastra, “The treasury is the backbone of the State.” A weakened treasury ultimately weakens governance itself.

When Accountability Becomes Selective

One of the most persistent criticisms of India’s financial governance concerns unequal enforcement.

Small borrowers frequently experience swift recovery proceedings.

Farmers face repeated notices over modest defaults.

Micro, small and medium enterprises often encounter relentless scrutiny before receiving credit.

In contrast, influential economic offenders have repeatedly demonstrated remarkable ability to restructure liabilities, prolong litigation and relocate across international borders before decisive action materialises. Whether this perception is entirely accurate or not, it significantly influences public confidence.

Justice must not merely be done.

It must be seen to be done with equal rigour, irrespective of wealth, status or influence.

The rule of law derives legitimacy from equality, not discretion.

Reforming the Republic’s Banking Architecture

Recovering fugitives addresses the consequence.

Preventing future frauds addresses the cause.

The lessons emerging from the Punjab National Bank episode are therefore unmistakable.

Every international financial transaction must remain fully integrated with domestic banking systems in real time.

Artificial intelligence and predictive analytics should identify abnormal transaction patterns before they become catastrophic.

Concurrent auditing should evolve from routine procedural verification into dynamic risk-based supervision.

Boards of public sector banks must be insulated from undue influence while strengthening professional accountability.

Whistle-blower protection must become meaningful rather than symbolic.

Regulators should increasingly emphasise preventive supervision instead of post-facto correction.

Technology must serve transparency.

Governance must reinforce technology.

Neither can substitute for institutional integrity.

The Moral Economy of Public Trust

Banks survive because citizens believe in them. Depositors entrust their lifetime savings not to buildings of concrete and steel but to systems of accountability. Every cheque honoured, every digital payment completed and every loan sanctioned ultimately rests upon one invisible foundation—trust.

Once that foundation weakens, recapitalisation alone cannot restore confidence.

Financial institutions require not only capital adequacy but also moral adequacy.

Integrity is the most valuable asset appearing on no balance sheet.

Editorial Verdict: Returning the Fugitive is Not Enough

If Britain ultimately extradites Nirav Modi, India will undoubtedly celebrate an important legal and diplomatic achievement. It will affirm that economic offenders cannot indefinitely evade accountability through geographical distance or prolonged litigation.

Yet the Republic must resist the temptation to regard extradition as the culmination of justice.

It is merely its commencement.

The larger verdict concerns institutions rather than individuals.

The Nirav Modi affair is fundamentally the story of a banking system that ignored warning signals, an administrative culture that responded too slowly, regulatory mechanisms that reacted after the event and governance structures that underestimated the sophistication of modern financial crime.

Britain may or may not return the Kohinoor.

It may soon return this “live diamond.”

But India’s true national treasure has never been a gemstone.

It is the faith of millions of depositors, taxpayers, pensioners, entrepreneurs and ordinary citizens who believe that public institutions will protect their savings with vigilance, impartiality and integrity.

That trust cannot be extradited.

It must be earned.

It cannot be auctioned.

It must be safeguarded.

It cannot be legislated.

It must be lived.

As the Roman satirist Juvenal posed a question that has echoed across two millennia:

“Quis custodiet ipsos custodes?” — Who will guard the guardians themselves?

Until India’s financial institutions answer that question with unwavering transparency, fearless accountability and uncompromising integrity, every recovered fugitive will represent not the end of a scandal, but merely the closing page of one chapter in a much longer history of financial governance.

For the ultimate jewel of any democracy is neither the Kohinoor nor a celebrated diamond merchant.

It is public trust.

Lose that, and no treasury can purchase it back.

M. Shiva Prasad, IPS (Rtd.) is a dedicated law enforcement professional who served the combined Andhra Pradesh cadre before opting for the Telangana cadre. Though a native of Andhra Pradesh, he considers himself a true Hyderabadi with an abiding love for the Telugu people. Driven by sincerity, fearlessness, and a lifelong fight against inequality and injustice, his ultimate strengths remain his goodwill and deep affection for the public and the police force. Today, he continues his mission by writing snippets and articles true to his conscience.

Email: Shivareach@yahoo.com

Mobile: 98480 38774